If a dishonest trader sells his goods at x% profit or loss on cost price and uses y% less weight, then his profit percentage or loss percentage will be:

× 100%

(Use + sign if goods are sold at x% profit and – sign if they are sold at x% loss.)

Concept 3

If a dishonest trader uses faulty weight of w units instead of r units and claims to make a profit of p%, then:

Real net profit percentage =

(in case the trader claims to make a loss, we will use - sign for p)

Note: if the formula evaluates to a negative value, it means there is a net loss.

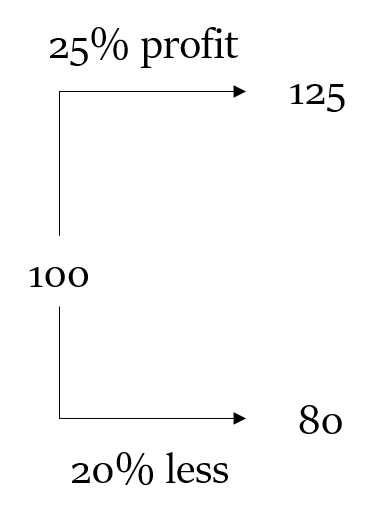

Q. A shopkeeper seems to sell an article at a profit of 25%. But, he uses a weight which is in reality 20% less than the weight indicated on it. What must be his real profit percentage?

Explanations :

Explanation 1: Traditional Method

Let quantity purchased be 1 kg for Rs. 1000.

But since he sold only 800 gm, the 200 gm that he saved will be his profit too.

Shopkeeper seems to sell an article at a profit of 25%. (this is first profit)

But, he uses a weight which is in reality 20% less than the weight indicated on it.

Now, we need to get back to 100. Difference remains the same, i.e. 20, but now the base will be 80.

The corresponding profit percentage = (20/80) × 100 = 25%

So, 20% less weight is equivalent to 25% profit. (this is second profit)

Required profit percentage = Resultant of two profits = 25 + 25 + (25 × 25)/100 = 50 + 6.25 = 56.25% (here we have just applied the formula of successive percentages)

Fraction Method

Shopkeeper seems to sell an article at a profit of 25%. (this is first profit)

But, he uses a weight which is in reality 20% less than the weight indicated on it.

20% = 1/5

Difference remains the same, but new base = 5 – 1 = 4

So, profit percentage = (1/4) × 100 = 25% (this is second profit)

Required profit percentage = Resultant of two profits = 25 + 25 + (25 × 25)/100 = 50 + 6.25 = 56.25% (here we have just applied the formula of successive percentages)

Explanation 3: Formula Method

Using formula 1

If a dishonest trader sells his goods at x% profit or loss on cost price and uses y% less weight, then his profit percentage or loss percentage will be = × 100%

The approaches and concepts discussed in this article are not limited to only problems with faulty weights, but in any problem where the amount sold and that charged for is different.

Some More Questions

Q. Which of the following trick would maximize the profit of a businessman, when he sells a certain item?

I. Sell that item at 8% profit II. Use an incorrect weight which is 100 grams less than 1 kg, but is marked as 1 kg III. Mix 10% impurities in that item and sell that item at cost price IV. Increase the price by 5%, and use an incorrect weight whose real value is 5% less than what is marked on it.

Select the answer using the correct code.

(a) I (b) II (c) III (d) IV

Explanation:

Case I: In the first case, it is directly given that the profit is 8%.

Case II: For second case, let the CP of 1 kg of item be Rs. 100 Then CP of 900 g of item= (100/1000) x 900 = Rs. 90 Hence, profit percentage = {(100 - 90)/90} x 100 = 11.11%

Case III: Let the CP of 1 kg of pure item be Rs. 100 If he adds 10% impurity, then CP of 1 kg = {(1000/1100) x 100} = Rs. 90.90 Hence, profit percent = {(100 - 90.90)/90.90} x 100 = 10.01%

Case IV: If he reduces weight by 5%, then cost price of 950g = {(100/1000) x 950} = Rs. 95 and SP = Rs. 105 Hence, profit percent = {(105 – 95)/95} X 100 = 10.52%